Blog /

Industry Insights

The 'ISP 2020' - Top 5 highlights for batteries and VPPs

August 25, 2020

Updated: Oct 25, 2022

Originally published on newenergy.ventures (Orkestra's predecessor).

The Australian Energy Market Operator (AEMO) recently released its Integrated System Plan (ISP) for 2020, intended to guide governments, industry and consumers on investments needed for an affordable, secure and reliable electricity grid.

Let’s be clear - this report is a big deal.

Not only is it the most comprehensive modelling exercises for Australia’s energy future ever undertaken, its findings confirm Australia is on a near unstoppable path towards a more renewable and decentralised energy future.

It also confirms our hunch that batteries and VPPs have a much bigger role in Australia’s energy mix, alluded to in our recent whitepaper on opportunities for batteries and VPP in the Australian C&I segment. But what does the ISP mean, in particular for energy storage and virtual power plants?

Here are the top 5 highlights.

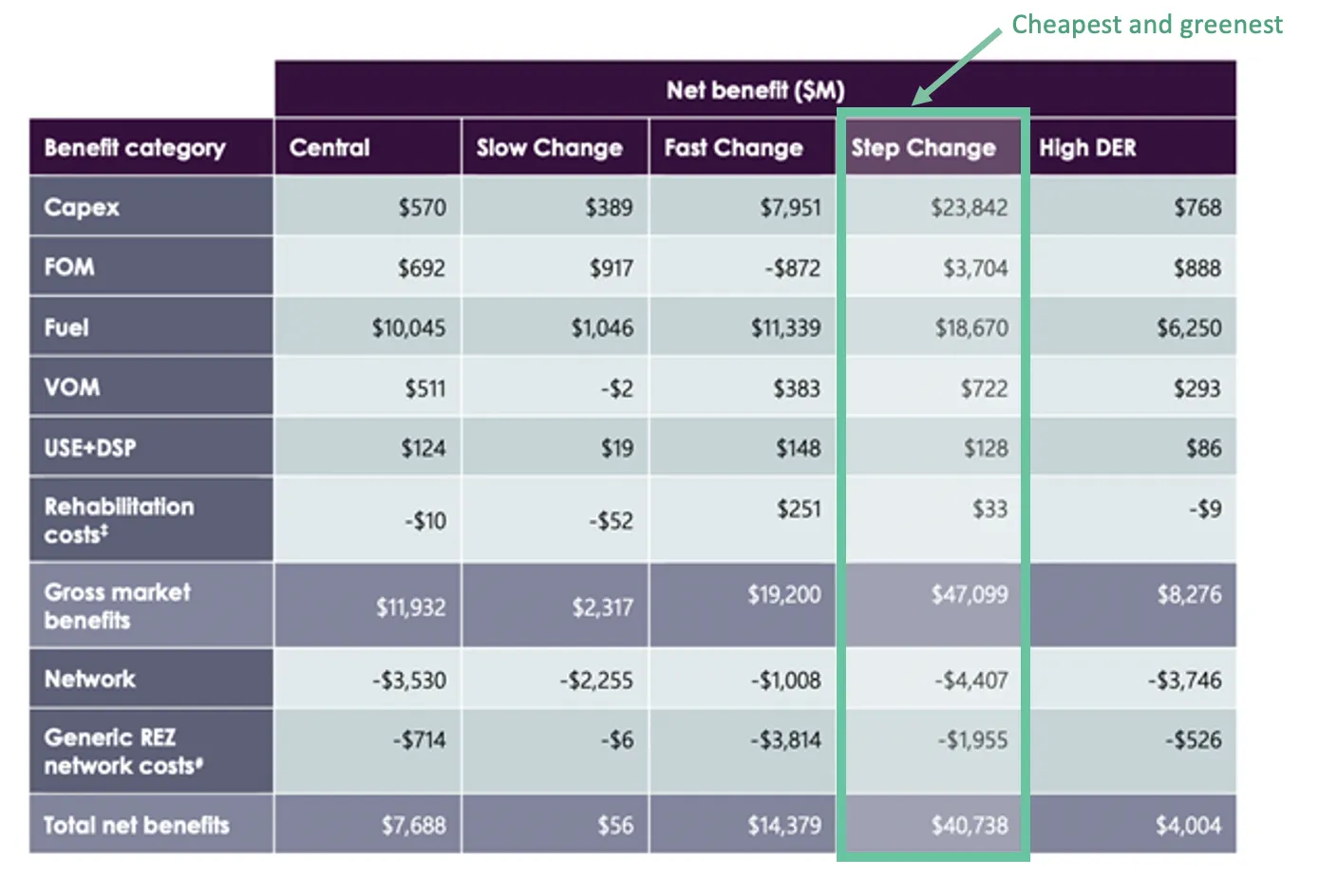

1. The cheapest option is the fastest, greenest option

Simply put, going green as fast as possible is the cheapest option for Australia’s future energy system. The net-benefit to Australia will be around $41 billion (with a ‘B’!) versus our system continuing to operate BAU.

If this report had been written even 5 years ago or by any other author, it would have been dismissed by some quarters as a progressive’s fever dream. But the author is the AEMO, an organisation known for providing conservative predictions and the modelling is strictly driven by lowest cost modelling.

Table 1 - Scenario analysis showing benefit of transmission investment (NPV, $ million)

For scenario definitions, jump to the end of this article.

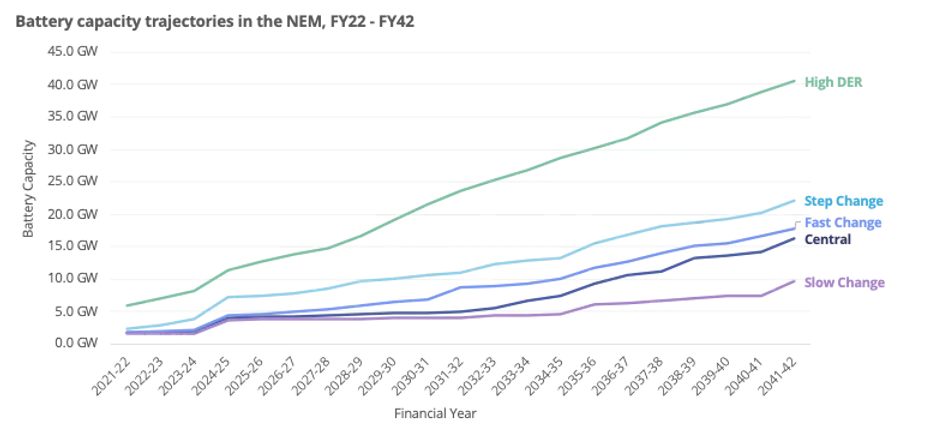

2. The battery market in Australia is expected to be huge

AEMO have modelled up to 40GW of batteries being deployed in the NEM under the high DER scenario and 22GW under the Step Change scenario. Even the vanilla central scenario shows 16.2GW by financial year 2042.

Figure 1 - Battery capacity trajectories in the NEM. Source: ISP Chart Data, NEV Analysis

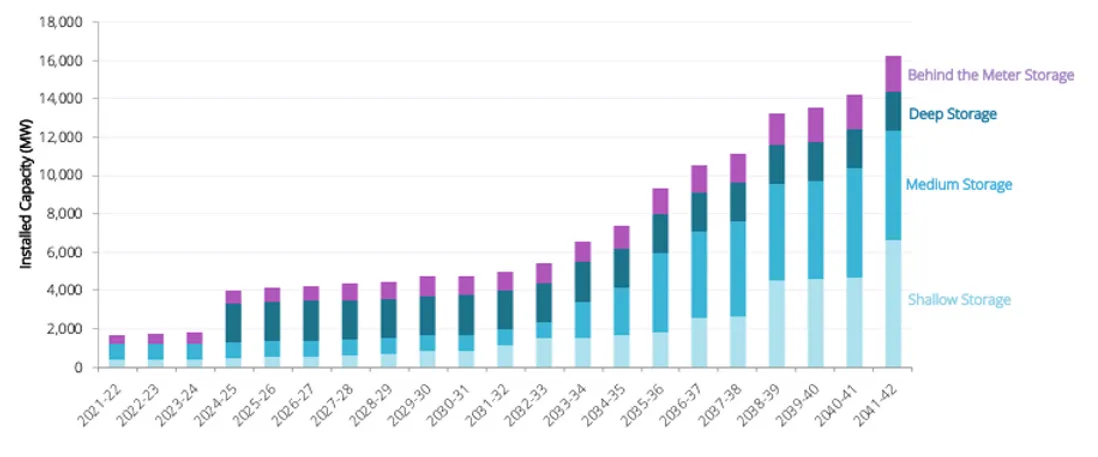

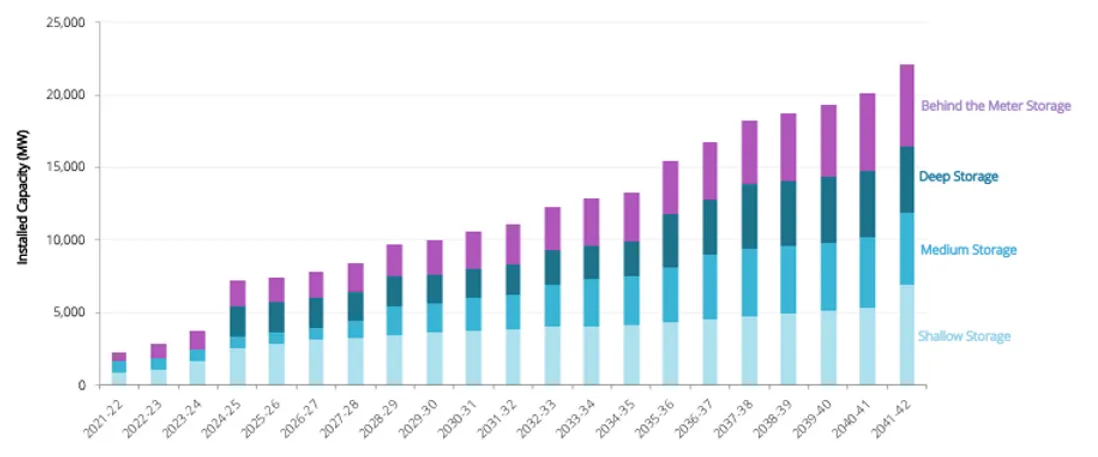

3. You don’t need as much deep storage as you might think

AEMO considered three kinds different kinds of dispatchable storage in their projections:

- Shallow storage, which includes VPP battery and 2-hour large-scale batteries. The value of this category of storage is more for capacity, fast ramping and FCAS (not included in AEMO’s modelling) than for its energy value.

- Medium storage, which includes 4-hour batteries, 6-hour pumped hydro, 12-hour pumped hydro, and the existing pumped hydro stations Shoalhaven and Wivenhoe. The value of this category of storage is in its intra-day energy shifting capabilities, driven by demand and solar cycles.

- Deep storage, which includes 24-hour pumped hydro, 48-hour pumped hydro, Snowy 2.0, and Tumut 3. The value of this category of storage is in covering VRE “droughts” (long periods of lower-than-expected VRE availability) and seasonal smoothing of energy over weeks or months.

Note that this dispatchable storage can exist in front-of-the-meter as well as within behind-the-meter batteries in VPPs. In addition to this, AEMO considered non-dispatchable storage which it coins as “behind-the-meter” storage.

In all but the Step Change scenario the only deep storage expected to be required is Snowy 2.0 as needed. Even then it will be dwarfed by the other storage options.

In our view this means that it is unlikely that other large storage projects will be committed to. It will be fast and easier for shallow and medium storage projects to be deployed. This will no doubt include more pumped hydro, but not much further to the scale of Snowy 2.0.

Central Scenario

Figure 2 - Forecast deployment of the battery storage under the Central Scenario. Source: AEMO ISP

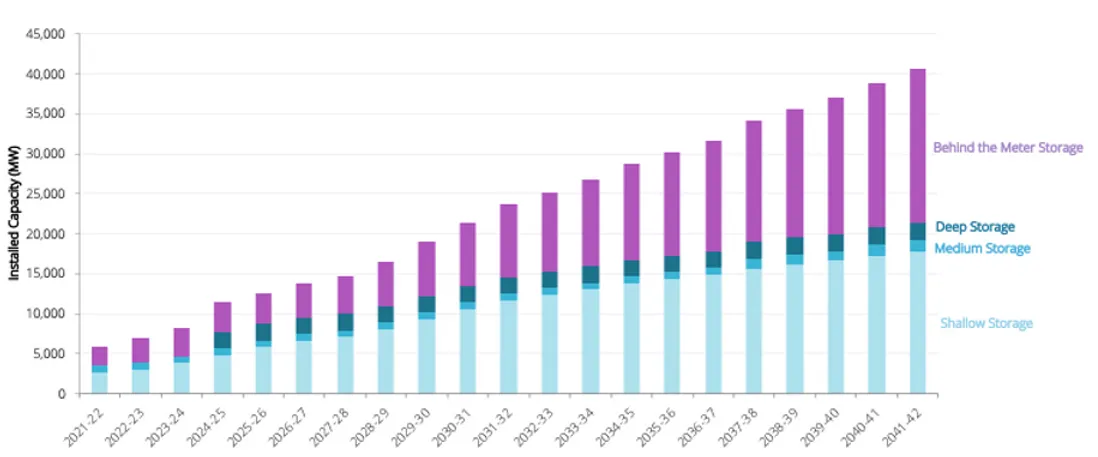

High DER Scenario

Figure 3 - Forecast deployment of the battery storage under the Central Scenario. Source: AEMO ISP

Step Change Scenario

Figure 4 - Forecast deployment of the battery storage under the Step Change Scenario. Source: AEMO ISP

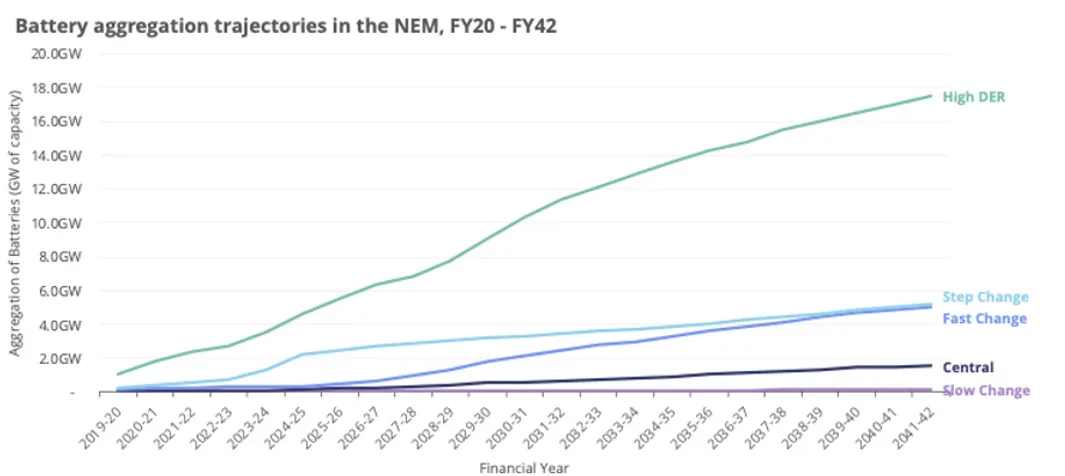

4. VPP could play a huge and vital role in the future grid

Hidden in the Input and Assumptions Workbook of the ISP is an incredible chart. It shows the various aggregation trajectory of battery storage in the NEM. AEMO predicts that by FY30, up to 9GW of aggregated battery storage could be operating in the NEM (i.e. the equivalent of 90 Hornsdale Power Reserves).

What is interesting is that AEMO does not appear to have modelled the full value stack for aggregated batteries, only their energy storage, capacity and ramping value. That is, they have not considered FCAS, network tariff savings or future value from fast frequency response and other value streams, and are therefore potential underestimating uptake.

Figure 5 - Aggregation trajectory for behind-the-meter battery storage in the NEM, FY20 – FY50

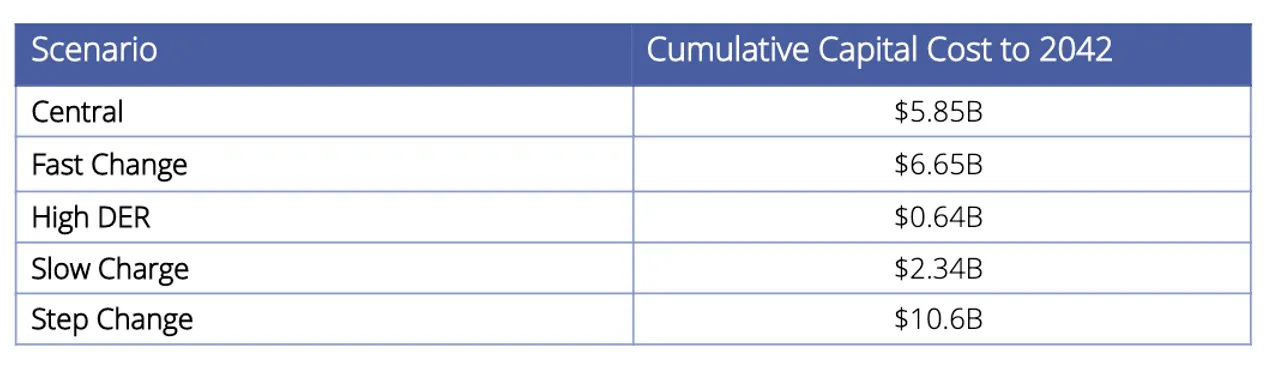

5. Front-of-the-meter energy storage could be a massive $10 billion market alone by 2042.

Hidden within the ISP Generation Outlook files is capital cost assumptions for the front-of-meter dispatchable storage.

This is the their forecast of market size for front-of-meter dispatchable batteries in Australia (i.e. does not include the costs of non-dispatchable behind-the-meter storage).

Table 2 - Cumulative capital cost to 2042 for grid-connected dispatchable battery storage

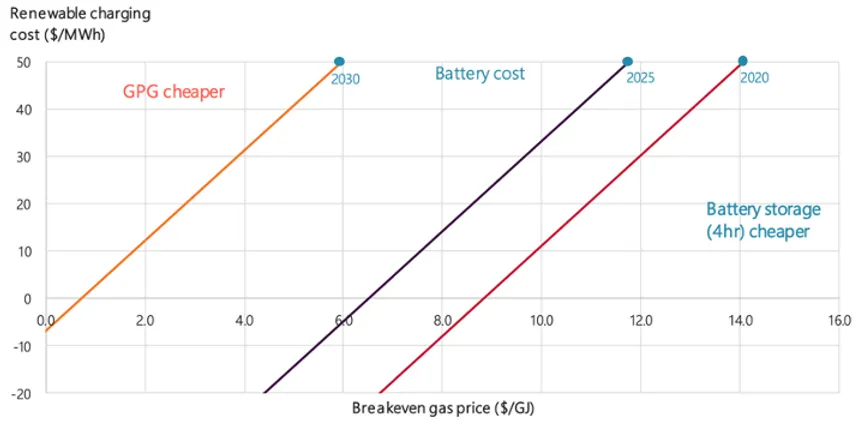

Bonus insight – It really blows to be a proponent of gas

What is so stark about the analysis is that there is no future role envisaged for fossil fuels except sometime in late 2030s where CCGT and gas peakier might get a tiny look-in. More to the point, retiring coal and gas generators will not be replaced by more coal and gas generators. The cheapest way forward is for coal and gas to be replacement by renewables and storage.

AEMO also drove a few extra nails into the coffin of gas, determining that gas needs to be $4-6/GJ to compete with renewable energy and storage by 2030 (see the chart below). The COVID commission has an “aspirational” target gas price of $6-7/GJ. This has been described as being “pie in the sky” targets. It would therefore seem that gas being a major part of Australia’s future generation mix is equally so.

Figure 5 - Aggregation trajectory for behind-the-meter battery storage in the NEM, FY20 – FY50.

In summary

The future is bright for batteries in Australia. In our view the step change scenario seems the most likely but is probably only realistic with a change of federal government.

But the report does not address the micro-economics of the battery and VPP value stack is the same way that we have done in our recent white paper. In our view, this leaves value on the table, especially from both reduced network investment, and correspondingly, behind the meter demand savings. This means we may see behind-the-meter batteries taking more market share than modelled here.

Appendix - the scenarios that AEMO considered

The five scenarios considered by AEMO span differing rates of change in technology development, renewable and distributed generation, decarbonisation policies, and the electrification of other sectors such as transport. These scenarios were developed through extensive consultation with industry. Scenario details:

- Central scenario - the pace of transition is determined by market forces under current federal and state government policies (see Page 32 of the ISP for details).

- Slow Change scenario - a slow-down of the energy transition, characterised by slower changes in technology costs, and low political, commercial, and consumer motivation to make the upfront investments required for significant emissions reduction. (NEV comment – does this feel likely to you??)

- High DER scenario - a more rapid, consumer-led transition, as consumers take control of their energy costs with easy-to-use, interactive technologies, falling costs for DER and EVs.

- Fast Change scenario - a more rapid technology-led transition, its costs reduced by advancements in grid-scale technology and targeted policy support. There is coordinated national and international action to reduce emissions that leads to innovation, automation, the accelerated exit of existing generators, and greater electric transport.

- Step Change scenario - both consumer-led and technology-led transitions occur in the midst of aggressive global decarbonisation and strong infrastructure commitments.

Figure 1 – Comparative rates of decarbonization and decentralization across the five ISP scenarios. NEV mark up.