Blog /

Industry Insights

Has Covid-19 crippled big-battery and virtual power plant economics

May 11, 2023

Big batteries in Australia have managed to get some serious momentum of late. Everyone has been inspired by the incredible economics of the early projects like Hornsdale Power Reserve, aka the Tesla big battery.

The value stack for battery-enabled virtual power plants (VPPs) and grid-scale batteries is typically built on a foundation of participating in the FCAS (frequency and ancillary services) market and wholesale market arbitrage. For a battery to do “wholesale market arbitrage”, it needs to buy electricity when it’s cheap and sell it when the price is high.

Simply put – batteries like the Hornsdale Power Reserve rely on price volatility in order to make money.

The ongoing Covid-19 pandemic has resulted in a substantial reduction in load and electricity prices for many grids across the globe. The Australian Energy Market Operator recently attributed potential morning peak demand reductions to COVID-19. Coupled with historical-low oil prices, COVID-19 has coincided with the lowest NEM quarterly average price since 2016. This decreasing wholesale energy price trend is set to continue based on projections by RepuTex.

But the average wholesale price is only one side of the story. What about market volatility? How COVID-19 has impacted volatility, and hence the opportunity for arbitrage, is not well understood. The AEMO recently observed mixed volatility across the NEM in Q1 2020, but what this means for batteries is still up in the air.

We set out to answer the question:

“Has COVID-19 affected wholesale market arbitrage opportunities across the NEM?”

To quantify this, we’ve used our Virtual Power Plant Economics Engine “Vippy" to analyse each calendar week of wholesale price data up until May 2020.

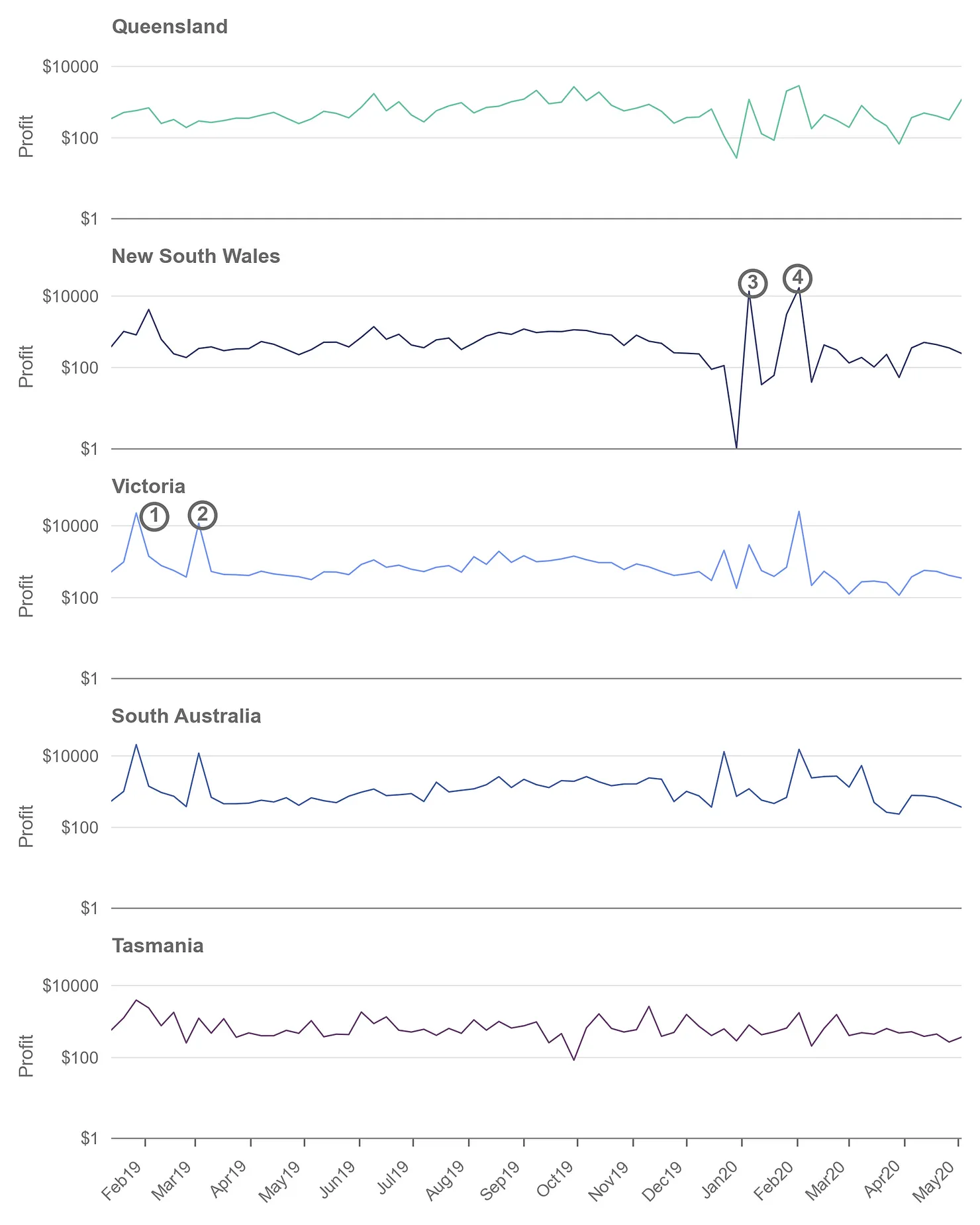

Figure 1 - Weekly wholesale arbitrage profit for a 1 MWh battery, by state.

Although we can see the last month or so has a downward trend in arbitrage profit for some states, the profit is still well within the bounds of what’s typical historically. This is confirmed in the graph below looking at average profit across all states.

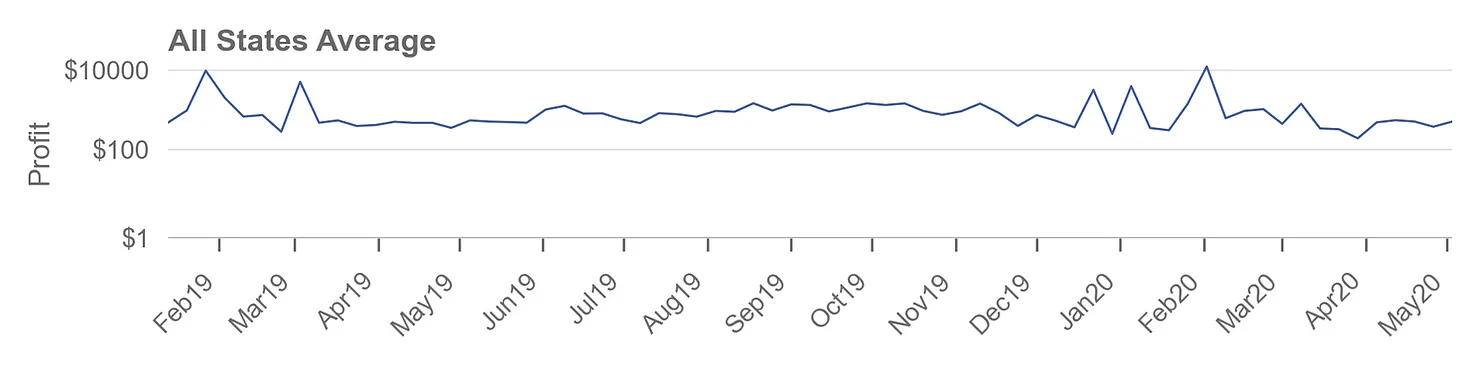

Figure 2 - Average weekly wholesale arbitrage profit for a 1 MWh battery for all NEM states.

In summary - no need to sell your lithium shares just yet!

What else does this data tell us about big-battery and VPP economics?

While we’re here, let’s look back at the last year. There are a few weeks that stand out as being exceptionally profitable that we’ve labelled in the graph. It turns out all of these events except for Event 2 have been recognised by the AEMO as high volatility events in their Quarterly Energy Dynamics reports.

- Event 1 on the 24th and 25th of January 2019 was caused by a combination of extreme heat, coal generator outages, and low wind generation in South Australia.

- Event 2 on the 1st of March 2019 was largely caused by extreme heat. As you’d expect, grid-scale batteries discharged heavily into this high price event.

- Event 3 on the 4th of January 2020 was caused by extreme heat and the separation of New South Wales and Victoria.

- Event 4 on the 31st of January 2020 was caused by extreme heat, coal generator outages, and the separation of South Australia and Victoria.

The weeks coinciding with these events were extremely profitable for big-batteries and VPPs, with our simulation indicating potential earnings of $23k, $12k, $14k, and $17k per 1 MWh of capacity, respectively. Pretty tidy! This is clear confirmation that wholesale volatility, in the sense used by the AEMO, corresponds to wholesale arbitrage opportunity.

It’s also interesting to see the zero profit week in New South Wales just prior to Event 3. Closer inspection of the wholesale data for this week shows that it was indeed an abnormally calm week.

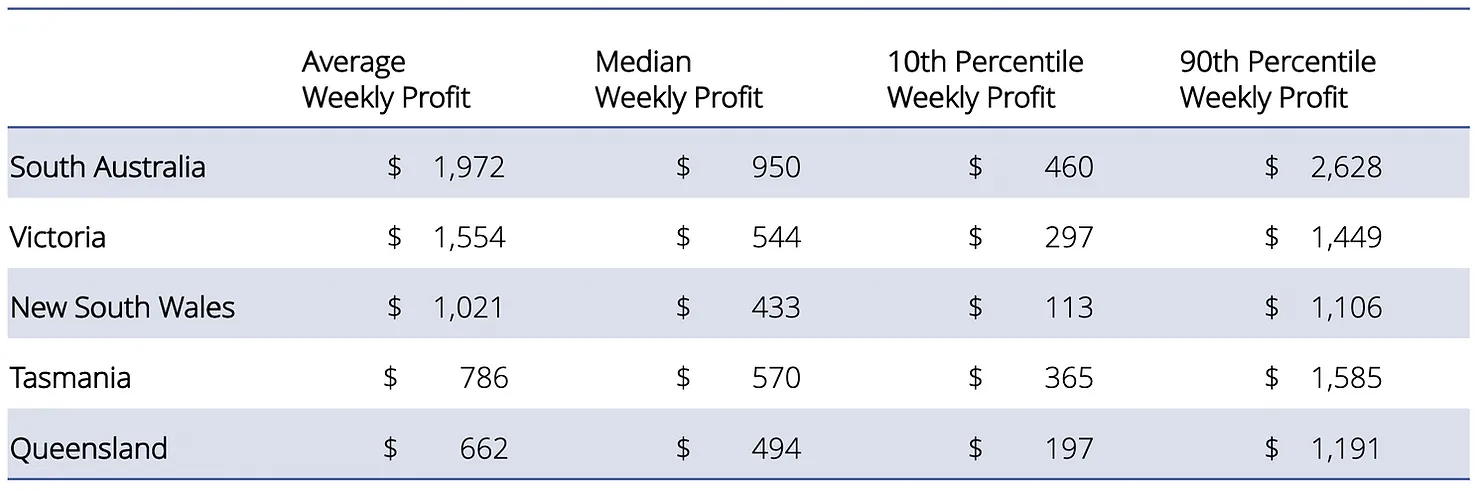

We can also use this data to rank the profitability of wholesale arbitrage in each state. To no one’s surprise, given its notorious volatility, South Australia comes out on top. What is a surprise, though, is that Queensland is the least profitable – behind even Tasmania with its highly dispatchable hydro fleet.Table - Average, median, P10 and P90 weekly profit per 1MWh battery capacity by state

In part two of this analysis, we plan to assess the impacts of recent wholesale price trends on the profitability of FCAS market participation. Stay tuned!