Blog /

Industry Insights

5 Things That Changed in NZ Network Tariffs This Year (and Why You Should Run the Numbers)

May 12, 2026

New Zealand's lines companies have released their 2026/27 network tariffs, and this year, it's not just the prices that moved. The structures did too.

Of the 28 tariffs in Orkestra Plan's NZ library that include demand charges, 25 increased the demand charge this year. Two tariffs introduced brand new demand charges. Powerco restructured entire tariff groups. Orion widened the peak-to-off-peak spread by 41%.

If you're selling or managing C&I sites with solar and batteries in New Zealand, any proposal built on last year's tariffs could need revisiting - and new projects will definitely need to utilise the latest tarrifs.

Here's what changed, and what it means for you and your customers.

What's driving the changes?

Two regulatory shifts are behind the numbers.

The Commerce Commission's DPP4 determination increased the revenue that lines companies can recover, giving them headroom to invest in the grid as New Zealand electrifies. And the Electricity Authority's Distribution Connection Pricing Reform, effective 1 April 2026, is pushing distributors toward more cost-reflective pricing.

At the same time, the demand picture is changing fast: more EV charging, more distributed generation, more pressure on aging networks.

The result? Tariff structures are shifting to match, and if you're designing solar and battery systems for C&I customers, the economics just changed.

You can find all the new tariffs live in Orkestra now. Log in to start applying these to your next C&I solar and battery project

Get your 3 week free trial

Get started exploring energy project feasibility analysis and reporting. Sign up now - no credit card required.

Sign up today1. Demand charges are up — across almost every network

This is the headline trend.

Of the 28 NZ tariffs that were in Plan from FY25 that include demand charges, 25 increased the demand charge this year. Two tariffs added brand new demand charges.

The standout numbers:

- Powerco (300+ kVA tariffs): demand charges doubled

- Unison: demand charges up 28.2% on average, with Anytime Maximum Demand (AMD) charges up 50%

- Vector: demand charges up 8.5% on average

What does that mean in practice? Higher demand charges mean the payback on peak-shaving just got shorter. A battery that clips demand spikes is now saving your customer more per kW than it was twelve months ago. Projects that were borderline last year may now stack up.

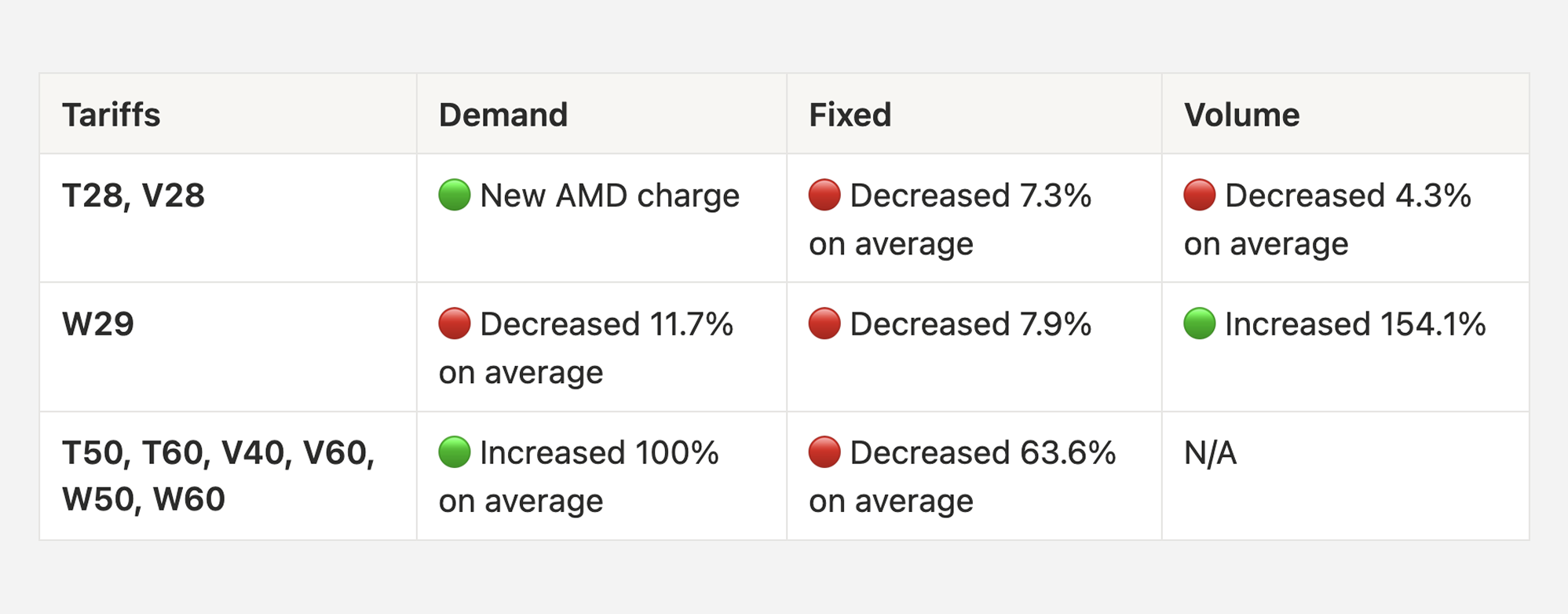

2. Powerco restructured key tariff groups — and the economics flipped

If you have projects on the Powerco network, pay attention. This isn't a simple price adjustment, Powerco has restructured key C&I tariff codes, changing the balance between demand, fixed, and volume charges.

T28 and V28 now include a brand new AMD charge of $0.10/kW/day. Time-of-use (TOU) volume rates have come down, narrowing the peak-to-off-peak spread. The net effect? These tariffs now reward consistent demand management more than shifting consumption between time periods. A battery system that reduces your customer's maximum demand, charging during low-demand periods and discharging to shave peaks, directly reduces that new AMD charge. If you're proposing batteries on these tariffs, that AMD saving needs to be front and centre in your business case.

W29 has gone the other direction. Demand charges are down ~12%, but volume rates have increased by 154%. That's a massive shift toward volume-based pricing, and it changes the economics entirely. Solar self-consumption and battery arbitrage become much more valuable when the customer is paying that much more per kWh. If you've got a W29 site in your pipeline that didn't justify a battery before, it's worth re-running.

The 300+ kVA tariffs (T50, T60, V40, V60, W50, W60) have seen demand charges double while fixed charges dropped 36–82%. The signal is clear: the network wants large users to manage their peak demand, and it's prepared to lower the entry cost to make that trade.

Here's how it breaks down:

If you're quoting a site on Powerco, last year's "best" tariff may not be this year's best tariff. Run the comparison before you send the proposal.

3. Orion widened the peak-to-off-peak spread by 41%

Orion is moving toward long-run marginal cost (LRMC) pricing for large general connections. In practice, the gap between what your customer pays at peak and what they pay off-peak just got significantly wider.

A 41% increase in the peak-to-off-peak spread strengthens the case for both solar and batteries. Solar self-consumption during peak periods offsets a higher rate. Battery arbitrage, charging when prices are low, discharging when they're high, captures a bigger spread.

If you have an Orion site in your pipeline with flexible load or storage potential, model it against the new tariffs. The returns may have moved meaningfully.

4. Wellington Electricity pushed fixed charges up hard

Wellington Electricity has increased charges across the board, but fixed charges stand out: up 23.6% on average, with one tariff increasing by 28.7%.

When a larger share of the network bill is fixed, the portion your customer can actually influence through solar or battery systems gets smaller. That doesn't mean projects don't stack up, but it changes the maths.

If you're building proposals for Wellington sites, make sure you're modelling the updated fixed-to-variable ratio so your savings estimates are accurate.

5. Unison is penalising peaky demand more aggressively

Unison's AMD charges are up 50%. Across all demand charge types, Hawke's Bay, Rotorua/Taupō, summer and winter peaks, the average increase is 28.2%. Fixed charges are up too (18.5% on average), but the demand signal is the story.

If you have Unison sites with peaky load profiles, the cost of those spikes just increased substantially. Battery storage for peak-shaving is the obvious play, and the business case just got stronger.

What should you do right now?

Two things.

First, ensure you're modelling C&I projects with the latest Tariff structures. The shift toward higher demand charges and wider TOU spreads changes which solar and battery configurations deliver the best returns, whether that's peak-shaving on a Unison AMD tariff or arbitrage on Powerco's restructured W29. If you're an Orkestra user - you can find the latest tariffs already uploaded and ready to use in the platform.

Second, re-visit existing deployed systems to see if there is a better tariffs now available to suit the site. With this much structural change, especially on the Powerco network, the tariff code a site was on last year may no longer be the cheapest option. If you quoted a customer in March, the numbers have already moved.

Here's a concrete example: a site on Powerco's W29 tariff that looked marginal for battery storage last year might now have a strong case, because the 154% volume rate increase means every kWh of solar self-consumption or battery discharge is worth significantly more. The only way to know is to run the numbers!

How to access the new tariffs in Plan

All 38 FY26/27 NZ tariffs are already in Plan's library. Here's how to use them.

To apply the new tariffs to a project:

- Create a project in the NZ market (or open an existing one).

- In the Site Baseline, go to the Tariff section and select Add Network tariff.

- Under the start date dropdown, select 'Current tariffs', you'll automatically be shown the correct FY26/27 tariffs based on your site's eligibility criteria.

To compare FY25/26 tariffs with FY26/27 tariffs side by side:

- Open your scenario and click Tariff changes.

- Make sure Include baseline tariffs is enabled.

- Click + New tariff group.

- Add the FY26/27 tariff as the network tariff.

- Use the baseline retail tariff for this group.

This lets you see exactly how the tariff change affects payback, cash flow timing, and overall returns for your specific site, so you can decide whether to update your proposal before it goes out.

The network tariff landscape in New Zealand is shifting. Make sure your proposals have shifted with it. Log in and run a comparison now

Book a Demonstration

Book a meeting with the Orkestra team in your region

Frequently asked questions

1. What NZ network tariffs are available in Orkestra Plan?

Plan includes 38 NZ network tariffs for the 2026–27 financial year, covering Vector, Powerco, Unison, Wellington Electricity, and Orion. All tariffs are effective from 1 April 2026 and can be selected directly from the tariff library without manual data entry.

2. How do I compare last year's NZ tariffs with this year's?

In Plan, open your scenario and click "Tariff changes." Enable "Include baseline tariffs," then add a new tariff group with the FY26/27 network tariff. You'll see the financial impact of the tariff change on your specific site, side by side.

3. Which NZ lines companies increased demand charges the most?

Powerco's 300+ kVA tariffs saw demand charges double. Unison's Anytime Maximum Demand (AMD) charges increased by 50%, with an average increase of 28.2% across all demand charge types. Vector's demand charges increased by 8.5% on average.

4. Do the new NZ tariffs change the business case for C&I batteries?

In most cases, yes. Higher demand charges strengthen the payback on peak-shaving battery systems. Wider TOU spreads, like Orion's 41% increase in peak-to-off-peak pricing, improve the returns on battery arbitrage. The specific impact depends on the site's load profile, location, and tariff, which is why modelling against the actual FY26/27 rates matters.

5. What is the Electricity Authority's Distribution Connection Pricing Reform?

The Electricity Authority's Distribution Connection Pricing Reform, effective 1 April 2026, requires NZ distributors to adopt more cost-reflective pricing methodologies for network connections. Combined with the Commerce Commission's DPP4 determination, it's driving the structural tariff changes visible in the FY26/27 rate schedules.