Blog /

Industry Insights

5 reasons why C&I virtual power plants will ultimately do better than residential ones

October 23, 2020

Updated: Oct 25, 2022

Originally published on newenergy.ventures (Orkestra's predecessor).

In the last few years we have seen a large number of residential virtual power plants (VPP’s) either being established or in the process of being established with nearly every major energy retailer and battery provider kicking the tires on the opportunity.

In many ways this is no surprise, given in that in Australia:

- We lead the world in per-capita uptake of residential solar

- We have the world’s largest market for residential batteries,

- Grid-connected energy storage has been demonstrated to be spectacularly lucrative, and...

- Traditional energy companies, battery vendors, controls providers and aggregators alike are all looking at each other's turf with keen eyes on its greenness.

But the focus on residential VPPs without an equal or greater focus on commercial and industrial (C&I) VPPs is somewhat of a surprise to the New Energy Ventures team. This comes off the back of writing a white paper on the best opportunities for batteries and VPP in the Australian C&I segment where we determined that VPP-enabled batteries are economically viable in large portions of Australia.

Below are the top 5 reasons why we think that C&I VPPs will ultimately outperform residential VPPs by being bigger and more valuable.

1. C&I VPPs can achieve scale easier

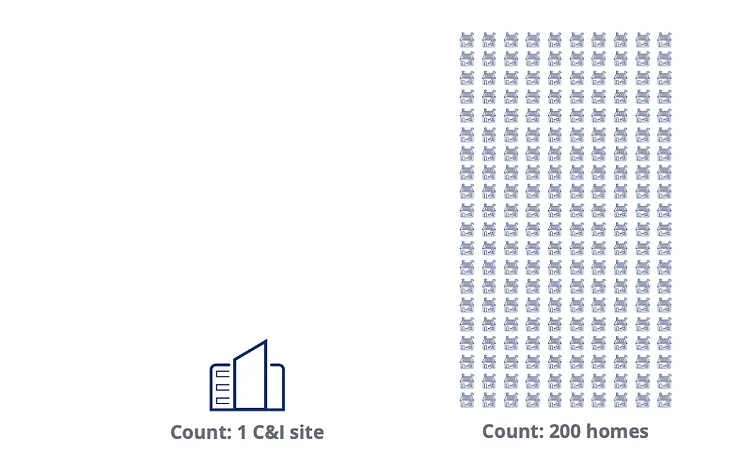

The first reason is a matter of simple scale. Scale is important for VPPs where scale is measured in terms of power (kW) not energy (kWh). For example the Contingency FCAS markets require a minimum offer quantity of 1 MW, and increments of 1MW. For the Reliability and Emergency Reserve Trader scheme (RERT) the minimum offer-able aggregated quantity is 10MW.

These thresholds could be met through the participation of a single large C&I battery but require hundreds of residential batteries to participate to achieve the same scale. With only some exceptions, most residential batteries only have a maximum continuous power output of just 3 - 5 kW.

Figure 1: Comparison of numbers of C&I versus residential participants for a 1MW VPP (realistic best case scenario for both)

This scale issue manifests itself in a number of ways: higher hardware costs, greater contractual overheads, increased sales costs, the need for customer service teams to manage customers and more complex coordination.

2. C&I VPPs have more complimentary battery value stacks

The second issue is the nature of the value stack for residential versus C&I batteries. Generally, the primary motivator for a residential customer to install a battery is to increase solar self-consumption. This can be driven by a simple desire for energy independence (i.e. non-commercial rational) or because using stored solar energy (versus exporting solar for meager feed-in rate) results in positive return on investment over time (i.e. commercial rational).

However, this means that the residential VPP-enabled battery value stack results in:

- High utilisation of the battery that reduces its life (>= 1 cycle per day)

- Conflict between the economic priorities of the household (i.e. solar storage) and the economic priorities of the VPP-provider (e.g. load shaping, FCAS participation, etc) due to differing preferred states of charge (Refer Figure 2 Below). For example, for the household to get maximum use out of the battery for solar storage, it is ideally empty at the start of each day so it can be charged with energy from the solar system. But VPP providers will likely prefer the battery to be (at least) half full so that it doesn’t miss any market events by having an empty or busy battery. These needs are partly resolved through accurate forecasting and co-optimisation but inherently in unresolvable conflict.

By comparison, C&I VPP-enabled battery value stack is:

- Built up of low energy throughput value streams (demand charge reduction, wholesale market arbitrage and contingency FCAS markets participation) resulting in extended battery life (< 1 cycle per day)

- Has little to no conflict been the value streams due to the same preferred states of charge

- Capable of reducing peak demand charges, which is comparatively more valuable (in $/kWh terms) than storing solar energy.

In summary, a battery at a C&I site can be VPP-enabled with less potential or actual contest for battery control from the different value streams.

Figure 2: Comparison of residential and C&I VPP-enabled battery value stacks

3. A residential VPP can be derated depending on when a ‘call event’ takes place

This next issue is far more technical, but a significant issue for residential VPPs is being able to get the power to the grid when it is needed.

First, some context. For an ‘event’ to be monetised, a change in battery state (charging or discharging) must take place. For example, if you wish to participate in a network-run demand response program, wholesale price arbitrage, or the contingency FCAS markets, a battery must automatically respond to a ‘call event’ by changing the power (kW) at which the battery is charging or discharging. The battery's ability to monetise / capture various services is highly dependent on the battery's current state, both in terms of the power it is charging/discharging at (kW) and how much energy it has stored in the tank (kWh).

But here’s the catch. The average residential solar system size in Australia is now around 7kW, but many residential solar systems have export limits of 5kW (or less) or battery systems are DC-coupled to the same “hybrid” inverter (i.e. this don’t have their own inverter which is AC-coupled). Furthermore, for reasons of cost-efficiency, inverters are sized to match peak solar output, not the combined peak output of the solar and battery. When a solar system is generating at full capacity and the residential load is typically low (in the middle of the day), the solar will hog the export and/or inverter capacity of the site limiting the ability of a battery to participate in market events. This means that a residential VPP must be dynamically derated as shown in the case studies below. A similar problem can constrain the ability of the battery to export to the grid at its full capacity in the evening.

Figure 3: Case studies of dynamic derating of battery export during market events. Assumptions - solar size: 5KWp, battery size: 5kWp, export limit: 5kW

Comparatively, commercial solar is usually sized to match commercial loads so there is minimal grid export (10-15%) and batteries are small relative to the load and AC-coupled, meaning the same issue is not as prevalent.

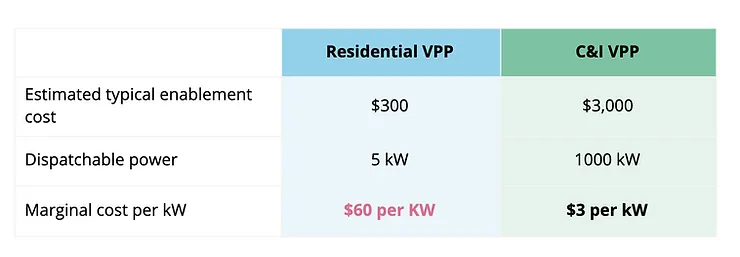

4. The marginal cost of enablement for C&I VPP is lower than for residential VPP (due to fixed costs)

Due to fixed costs of VPP enablement (controls, comms, setup, configuration and admin costs), the marginal cost of enablement for a residential VPP is very high.

Table 1: Comparison of enablement costs for residential and C&I VPP

5. A C&I battery can access the wholesale market without needing to link a battery (or VPP) investment to a specific energy retailer

A major drawback of the residential VPP solution is that once you have your VPP kit installed, you are locked into a specific retailer if you wish to participate in the wholesale market or FCAS markets. It is very impractical (but not impossible albeit with substantial trade-offs*) to delink energy retail when tapping those revenue streams. So if you participate in AGL’s VPP, your retail pricing and your VPP participation will both be via AGL. Naturally retailers love this, but it reduces choice for customers, and amplifies the (already) complex process of comparing offers between retailers. If Retailer A has higher energy rates but a better VPP payment than Retailer B, how is a consumer to know which retailer will result in the lowest cost for them? Often the details are in the T&C’s of the VPP agreement, and are difficult to compare.

C&I customers can participate in these markets more easily. The reason is complex, but it is related to a more complementary value stack. With a C&I customer, the battery is being employed primarily to target peak demand events (and not solar-self consumption), which lends itself to commercial structures that don’t bind the VPP-participation with a given site’s energy retailer*.

*Ask us how

** ShineHub does offer a BYO retailer VPP, however it taps revenues through network-initiated demand response programs. It is not (as we understand) participating in FCAS or wholesale energy markets.

Summary

While commercial energy storage and VPPs are yet to really prosper, we expect that to change as the market matures. There are plenty of opportunities for new VPP providers to step into the market and come up with new ways of sharing risk and reward that will likely unlock the C&I battery and VPP market.